Massachusetts is set to implement new changes for the ST-9 and ST-MAB-4 2022 sales tax forms. The changes include a new section to allow filers to report advanced payments. Advanced payments, in tandem with current tax due, will allow taxpayers to true-up any unaccounted liability. The change to the 2022 ST-9 form will be shown on lines 8 and 9.

Massachusetts advanced payments are calculated by: (1) total tax collected between the 1st and 21st of the previous month, or (2) at minimum, 80% of the prior month’s liability. Advanced payments must be paid by the 25th of the following month.

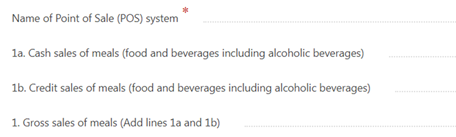

In addition to the ST-9 changes, Massachusetts has also updated the ST-MAB-4 which is used for reporting meals, prepared food, and beverage tax. The changes require taxpayers to distinguish sales on a cash and credit basis. The Massachusetts Department of Revenue will allow estimations for cash and credit sales until June 2022. Also, a new section on the return will require filers to list the point-of-sale system (POS) from a pull-down menu. Included with the changes mentioned above, Massachusetts will no longer require alcohol sales to be reported separately on the ST-MAB-4.